In the replica e-commerce industry, payment processing is one of the most critical components. Over the years, it has evolved through several major stages:

①. Offline Remittance and Bank Transfer Era (Pre-2005)

Before 2005, during the early phase of cross-border commerce, the global market had not yet established a mature, safe, and reliable online payment system. Most transactions were conducted through traditional offline remittance and manual bank transfers.

Popular methods during this period included:

-

Bank Transfers

-

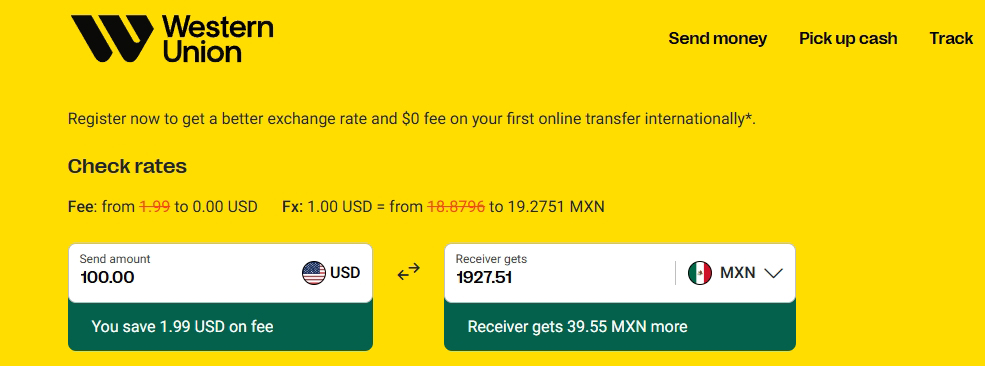

Western Union

-

MoneyGram

-

Credit Invoicing

-

Telegraphic Transfer (T/T)

These methods often involved long processing times, complicated procedures, and low operational efficiency. Additionally, they offered limited protection for both buyers and sellers, making the overall transaction process cumbersome and high-risk.

In recent years, WISE has become a popular option for international payments. Although it is a modern solution, it still falls under the category of offline bank transfers. Its growing adoption highlights the continued relevance of bank-based remittance methods in global e-commerce.

②. Third-Party Cross-Border E-commerce Platforms (2010–2016)

During the early golden years of global e-commerce, platforms like Alibaba International, AliExpress, eBay, Wish, DHgate, and Amazon experienced rapid growth. At that time, platform regulations were still evolving, and many sellers leveraged these platforms to process orders with fewer restrictions. Payments were typically completed through ESCROW-based third-party payment gateways, offering buyers and sellers a level of transactional protection. This phase lasted roughly from 2010 to 2016, marking a significant shift from traditional offline transactions to more streamlined and secure online payment systems.

③. Credit Card Payment Gateways (Post-2016 Shift to Own e-commerce Sites)

Around 2016, the landscape of cross-border e-commerce underwent a major shift. Major platforms began strictly enforcing intellectual property regulations, leading many sellers to move toward operating their own replica e-commerce own e-commerce websites. During this period, credit card payment gateways became the primary method of processing transactions.

To maintain transaction stability, chargeback rates were required to stay between 1% and 3%, while gateway commission fees typically ranged from 5% to 10%. In mainland China, several well-known gateway providers emerged, including Qianhai, DingPay, and Zhonghuifu, among others. However, the industry was riddled with risks: many providers withheld payouts, and some even disappeared with client funds, leading to significant financial losses for merchants.

In short, while credit card processing was technically available during this period, sellers in niche or high-risk product categories faced serious risks, including frozen funds and inaccessible revenue, often amounting to tens or hundreds of thousands of USD—with little to no legal recourse.

④. Current Situation: Payment Gateway Collapse Since Late 2018

Starting in the second half of 2018, the cross-border payment gateway industry faced a severe crisis. A surge of issues such as non-fulfillment of orders and Product not as described led buyers worldwide to initiate widespread payment disputes and chargebacks. This caused many payment gateway providers to suddenly shut down or disappear, severely damaging the entire ecosystem.

In response, major credit card networks implemented stringent risk control measures, resulting in payment approval rates plummeting—often below 30%, and in many cases falling under 10%. Essentially, the traditional payment gateway industry serving branded products, especially those involving top-tier and mid-tier brands, has been dismantled.

Today, there is no legitimate credit card payment gateway provider capable of processing payments for these kinds of goods. Claims promising such services are typically deceptive advertising aimed at collecting setup fees, and either the providers run away with funds or fail to deliver meaningful transaction success rates. Over 99% of these gateways cannot achieve even a 10% payment success rate.

In summary: For sellers operating parallel-market or niche e-commerce sites, relying on credit card payment gateways for receiving payments is no longer viable. Investing time or money in these solutions is highly likely to result in failure and wasted resources.

Nowadays, mainstream payment processing for replica-market e-commerce primarily relies on using Dual-site (A/B site) payment methods. Commonly adopted solutions include PayPal jump payment, Stripe jump payment , multi-gateway payment systems, and so on.

However, the A/B site setup is only a basic framework and is not sufficient on its own. Significant strategic work is required on top of this framework to optimize payment processing and overall operations.

I will cover these strategic approaches and related topics in detail in upcoming articles.

These systems support buyers making payments via bank cards, credit cards, PayPal, Stripe, and various local mainstream payment methods across different countries. This diversified payment approach helps merchants accept funds more smoothly while accommodating buyers’ preferred payment options worldwide.

![5 Best WordPress Themes for Replica Product International Trade Websites [Recommended]-Custom E-commerce Solutions for High-Quality Designer-Inspired Fashion Replicas | Website Development, Dropshipping, Payment Integration for PayPal and Stripe, Ad Cloaking Services](https://replicasmaster.com/wp-content/uploads/2025/06/1-1-220x150.jpg)